How Raleigh Rental Property Can Help Build Long-Term Retirement Wealth

When most people think about building retirement savings, they immediately think of 401(k)s, IRAs, and investment portfolios. While those are important, many rental property owners are building retirement wealth through another powerful asset they already own: their investment property. A well-managed rental property has the potential to generate monthly cash flow, appreciate in value over time, and gradually build equity as the mortgage is paid down — creating multiple sources of long-term wealth that can complement traditional retirement savings.

What You'll Learn in This Article

- How a rental property builds equity differently than a typical retirement account

- Why rental income often keeps pace with inflation

- How rental property can produce both income and appreciation at the same time

- What tax advantages come with owning rental real estate

- Why time and holding period matter so much to long-term results

- How rental property can fit alongside your other retirement accounts

Someone Else Is Paying Down Your Mortgage

This is the part that surprises people who haven't thought about it before. With a 401(k), growth depends on the market and how much you personally contribute. With a rental property, there's a third party doing some of the work: your tenant. Every rent payment doesn't just cover monthly income — a portion of that payment is gradually reducing your mortgage balance and increasing your equity. Over years, and especially decades, that principal reduction can become a significant source of wealth.

Example: What Could 20 Years Look Like?

Every property is different, but here's a simplified example to illustrate how a rental property can build wealth over time. This example is for educational purposes only and is not intended to predict future investment performance.

| Assumption | Example |

|---|---|

| Purchase Price | $400,000 |

| Down Payment | 20% ($80,000) |

| Loan Amount | $320,000 |

| Mortgage | 30-Year Fixed at 6.5% |

| Starting Monthly Rent | $2,800 |

| Annual Rent Increase | 3% |

| Annual Property Appreciation | 3% |

| Vacancy | 5% |

| Property Management Fee | 8% of collected rent |

| Annual Property Taxes | $3,600 |

| Annual Insurance | $1,200 |

| Annual Maintenance & Repairs | $2,500 (estimated) |

| Tenant Turnover Costs | ~$500/year (averaged; assumes turnover roughly every 3 years) |

After approximately 20 years, the owner may have built wealth through several sources:

| Source of Wealth | Illustrative Amount |

|---|---|

| Mortgage Principal Paid Down | ~$141,900 |

| Property Appreciation | ~$322,400 |

| Net Cash Flow Received | ~$147,700 |

| Estimated Total Wealth Created | ~$612,000 |

The important takeaway isn't the exact numbers — it's that rental property can build wealth in multiple ways at the same time. While tenants help pay down the mortgage, the property may appreciate in value and potentially generate positive cash flow, creating several sources of long-term financial growth.

This example is for illustration only and is not a guarantee of future performance. Actual results depend on purchase price, financing terms, rental income, operating expenses, vacancy, property condition, market conditions, appreciation, and how long the property is held. Cash flow and principal figures assume a fixed mortgage payment held constant over 20 years (no refinance) and operating expenses held flat rather than increasing with inflation; rent is assumed to grow 3% annually as shown above. Turnover costs are averaged over the holding period and will vary based on how often a property turns over and the condition of the property at move-out. This example assumes no major capital expenditures (such as roof replacement, HVAC replacement, or foundation repairs) during the 20-year holding period; these costs are unpredictable and vary widely by property. Tax benefits are not included because they vary by investor — please consult your CPA or financial advisor regarding your specific situation.

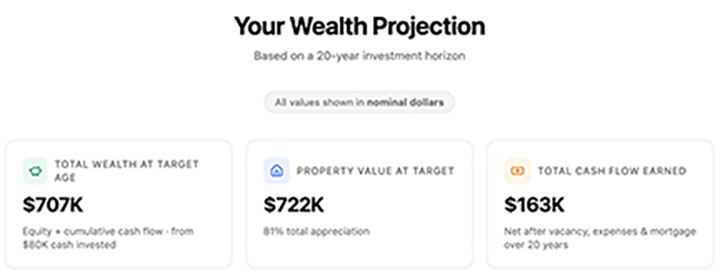

See What This Looks Like With Your Own Numbers

The example above uses fixed assumptions to illustrate the concept. Our free Rental Property Wealth Calculator lets you plug in your own purchase price, financing terms, and rent to see a personalized projection.

Rental Income Often Keeps Pace With Inflation

Fixed-income investments lose purchasing power over time — that's one of the harder truths about retirement planning. As home values and wages rise across Raleigh, Cary, and Durham, rents have historically tended to rise over time, although market conditions vary, which means a well-managed rental can help offset the rising cost of living rather than falling behind it.

You're Not Choosing Between Income and Growth

Most investments make you pick one: income now, or growth later. Rental property tends to deliver both. You're collecting rent today while the property itself appreciates. The Federal Reserve has tracked median home prices rising nearly 400% over the past 30 years nationally, and the Triangle's population and job growth have kept it among the stronger-performing regions in that broader trend.

Related Reading

Tax Advantages You Won't Find in a 401(k)

Mortgage interest, depreciation, property taxes, insurance, repairs — these are all deductible in ways that most retirement accounts simply don't offer. Many owners are able to offset a meaningful chunk of their rental income for tax purposes while the property keeps building value in the background. Worth a conversation with your CPA about how it applies to your specific situation, but the advantage itself is real. For more on how owner finances and reporting work day to day, see our Owner FAQs.

You Have More Control Than Many Other Investments

A stock portfolio asks you to trust market forces you can't control. A rental property is something you can walk through, improve, and actively manage. You choose the upgrades. You choose who manages it. That kind of control is rare among retirement assets.

Rental property doesn't have to replace traditional retirement accounts. Many investors use it alongside 401(k)s, IRAs, and other investments to diversify their retirement strategy. Because real estate often behaves differently than the stock market, it can provide another source of long-term income and wealth.

The Power of Time

The biggest advantage rental property has isn't necessarily appreciation or rental income — it's time. A property held for five years can perform very differently than one held for twenty. Mortgage balances decline, rents often rise over time, and appreciation has more time to compound. Many investors who achieve the strongest long-term results simply buy quality properties and hold them.

How Much Equity Can a Rental Property Build Over Time?

The amount of equity a rental property builds depends on the purchase price, financing terms, appreciation, and how long the property is held, but the underlying mechanism is consistent: every mortgage payment a tenant's rent covers reduces the loan balance, and rising property values add further equity on top of that. Using a simplified example of a $400,000 property held for 20 years, an owner could realistically see well over $400,000 in combined equity from principal paydown and appreciation alone, before accounting for any rental income along the way. Actual results vary by property and market, which is why working with a local expert who understands current Raleigh-area pricing and demand matters as much as the math itself.

Why Is Rental Property Considered a Good Retirement Investment?

Rental property is often considered a strong retirement investment because it can generate income from multiple directions at once. Rather than relying on a single source of growth, owners benefit from monthly cash flow, gradual equity buildup as tenants pay down the mortgage, potential appreciation over time, and tax advantages not available through most traditional retirement accounts. It's also a tangible asset that owners can actively manage and improve, rather than one that depends entirely on market performance. For investors looking to diversify beyond stocks and bonds, a well-managed rental property can provide a more stable, hands-on complement to a traditional retirement portfolio — particularly in markets like the Triangle, where population and job growth continue to support long-term rental demand.

The Difference Comes Down to Management

Rental property can be an excellent long-term investment — but it isn't completely passive. Owners who actually build wealth this way are the ones who hold long-term, price strategically, keep good tenants in place, and stay ahead of maintenance instead of reacting to it after the fact. That's the gap professional management is built to close — see our management pricing and owner guarantees for what that looks like in practice.

Related Reading

Ready to See What Your Property Could Be Worth Long-Term?

If you're weighing whether to hold a property for the long haul, understanding its current rental value is a good place to start.

Request a Rental Analysis Today✔ Rental pricing recommendations ✔ Local market insights ✔ Property-specific guidance ✔ No-obligation consultation

"The most successful rental property owners don't think about their property month to month. They think decade to decade. Equity, income, and appreciation compound quietly in the background, but only if the property is priced right, maintained well, and managed with that long-term goal in mind."

Robert Dell'Osso — CEO & Broker-Owner, MasterKey Property Management

The Bottom Line

A rental property can generate monthly income today while also building equity, benefiting from long-term appreciation, and providing potential tax advantages along the way. For many investors, that combination makes rental real estate an important part of a diversified retirement strategy.

If you're already working with us, this is exactly why we focus on protecting and growing your property's long-term value, not just keeping it filled.

Need Help Thinking Through Your Property's Long-Term Value?

MasterKey Property Management provides full-service property management throughout Raleigh and the Triangle — helping owners protect and grow their rental property as a long-term asset.

Learn More About Our Property Management Services

📞 919.655.3950

🌐 www.masterkeypm.com

.JPG)